Preferred Equity Explained

Preferred equity occupies an interesting position between debt and ownership.

It can provide additional capital while maintaining alignment between participants in the project.

Understanding how preferred equity functions can help clarify how sophisticated projects balance risk and return.

Mezzanine Financing Explained

Some real estate projects require more capital than senior lenders are prepared to provide.

Rather than increasing equity contributions, developers sometimes introduce mezzanine financing to bridge the gap.

Understanding how mezzanine capital interacts with other layers of financing can improve flexibility when structuring complex projects.

Senior Debt Explained

Senior debt is often viewed as the foundation of real estate financing.

It typically carries the lowest cost of capital, but also comes with the most defined lending parameters.

In larger projects, senior debt is rarely the only capital involved.

Understanding where senior financing fits within the broader structure can provide clarity when evaluating project feasibility.

Understanding the Capital Stack in Real Estate

Many people assume real estate deals rely on a single mortgage.

In reality, larger projects often involve multiple layers of capital working together.

Each layer has its own expectations, risk tolerance, and role in supporting the project.

Understanding how capital fits together can often be the difference between a project moving forward or remaining stuck at the planning stage.

Structure plays a much larger role in real estate than most people initially realize.

How Real Estate Projects Move From Private Capital To Bank Financing

Many real estate investors assume the goal is always to secure bank financing from day one.

In reality, many successful projects move through multiple stages of capital before reaching conventional lending.

Private capital often plays a role early in a project’s lifecycle — not as a permanent solution, but as a way to create momentum, reduce risk, and position the asset for stronger long-term financing.

Understanding how capital transitions from early-stage funding to institutional financing can open up opportunities that might otherwise appear out of reach.

I’ve written a new article exploring how experienced investors and developers think about sequencing capital and why structure often matters as much as rate.

If you’re involved in development, investment real estate, or commercial property, this may provide useful perspective.

Senior Debt Explained

Real estate developments in Canada are rarely financed with a single source of capital.

Behind almost every successful project is a carefully structured capital stack, where each layer of financing carries a different level of risk, return, and priority.

At the very top of that structure sits senior debt — the primary financing used to fund the majority of a project’s cost. Because it holds the first claim on the property, it represents the lowest risk position in the capital stack, but also comes with the most stringent underwriting requirements.

Understanding how senior debt works is critical for developers, investors, and professionals involved in commercial real estate.

In my latest article, I break down:

• What senior debt means in the Canadian lending environment

• How development loans are typically structured

• Why Canadian lenders take such a conservative approach

• Where senior debt sits within the broader capital stack

For anyone involved in development, capital raising, or structured finance, understanding this layer of capital is foundational.

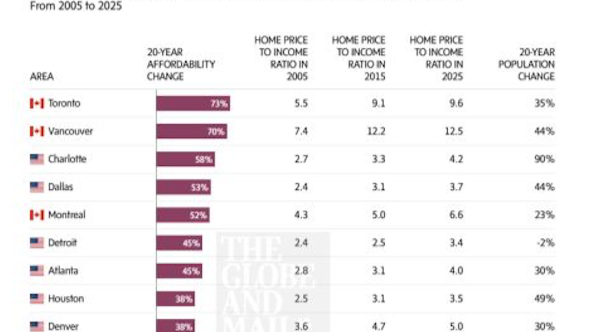

Canada’s Housing Market

Canada’s housing market is still adjusting.

New February data shows prices in both Greater Vancouver and the Greater Toronto Area remain below their 2022 peaks, with benchmark prices down roughly 6–8% year-over-year.

Is this just a market correction… or the start of a longer reset in Canadian housing?

I put together a short breakdown of what the numbers are telling us and what it could mean for buyers, sellers, and investors.

Take a look at the article below and let me know your thoughts.

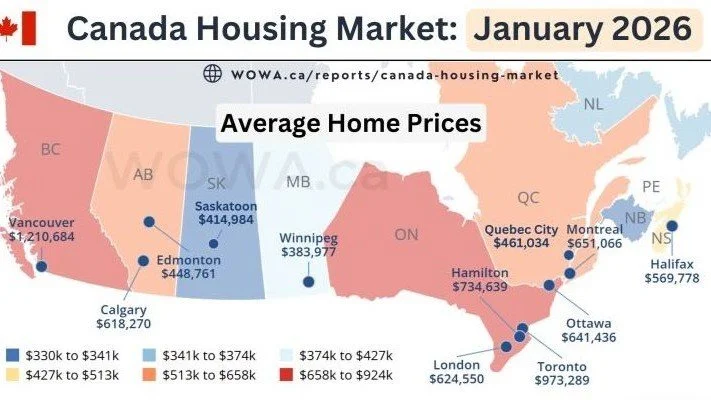

The Canadian Housing Market Has Shifted

For the first time in years, the biggest risk in real estate isn’t rising prices.

It’s making the wrong decision because you’re still using a 2021 strategy in a 2026 market.

The Canadian housing market didn’t crash to start the year — it recalibrated. Prices have eased, sales activity has slowed, and inventory has grown in many regions. In British Columbia, we’ve moved firmly into buyer-leaning conditions, and nationally the benchmark price has now declined for several consecutive months.

That’s not a crisis.

It’s a completely different environment — one that rewards planning instead of speed.

2026 Market Outlook

2026 isn’t about guessing the market.

It’s about building a smarter plan.

Lower rates, global opportunities, and real assets are creating new ways to grow and protect your money.

Read the article and learn how to position your investments for the year ahead.

2026 Market Outlook

Most people don’t realize their financial plan is being tested until it’s already under pressure.

As we move into 2026, markets are changing in ways that won’t be obvious from headlines alone. Concentration risk is higher, borrowing decisions are more complex, and the margin for error is shrinking — especially for those nearing retirement or managing debt.

I wrote this article because the 2026 Market Outlook highlights a critical shift: the next phase of markets will reward structure, discipline, and informed decision-making — not autopilot investing or hope-based strategies.

This isn’t a technical breakdown. It’s a practical read about what these changes mean for real people making real financial decisions — investments, mortgages, cash flow, and long-term security.

If you want to understand what’s changing before it impacts your plan, I strongly encourage you to read this.

The cost of reading it is a few minutes.

The cost of ignoring it could be far higher.